Yet another millennial-targeting, direct-to-consumer disrupter wannabe with cult-like followings…? Don’t brush them off. Legacy companies are taking notes as DTC brands seem to be outsmarting, outpacing, and outmaneuvering them. Jenny Chan, WARC’s China Editor, ruminates about their moves in this Spotlight series.

This article is part of a Spotlight series on what marketers can learn from DTC disruptors in China. Read more

A new genre of digital-native, contemporary brands we refer to as “DTC disruptors” in China have quickly eroded market share from big brands in their respective categories. They have typically filled gaps in the market, are nimbler in their organization structures, more adaptive to China's constantly changing consumer preferences, sell through WeChat stores and private groups via intimate relationships, and glean more first-party data to increase loyalty.

With more new waves of such contenders racing to meet consumer desires and proving to be attractive targets for venture capital (VC) funding, what key lessons can be learnt from their journeys for both aspiring upstarts and established incumbents?

DTC not just a business model but a way of thinking

The abbreviation “DTC” was coined by Western brands as a new business model unique to Western markets (think Casper, Allbirds, Warby Parker). But DDB China’s Laura Liang points out that it is not that new to Chinese consumers, in a market where digital infrastructure and e-commerce are mature and many digital-native brands were actually the pioneers practising the DTC model, such as the Taobao-born snack brand 3 Squirrels. Success is deeply rooted in connectivity (consumers are connected with products through digital and social channels like mini programs), and an ecosystem (built to generate growth from consumer data and supply chain agility).

DTC will extend beyond being "just a type of brand or business model" and become "a way of thinking about business" for every brand, marketer and entrepreneur, writes Liang. More and more DTC brands have already become mature brands and most are no longer satisfied to be just a “niche and chic” brand – they want to keep innovating to become something more.

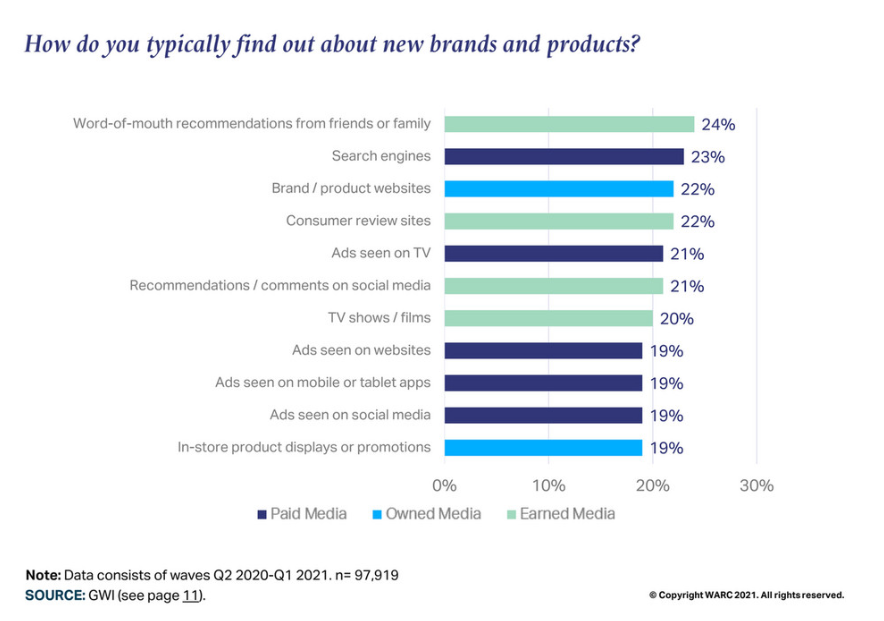

Earned media best for ‘brand new’ brand discovery

DTC Disrupters have brought in generous rewards for their early backers, but is the direct-to-consumer model truly sustainable for the China market, that is still heavily reliant on distributors, middlemen, platforms, and other in-between touchpoints that brands don’t own or have to shell out for?

Data from research firm GWI, surveying more than 90,000 Chinese consumers, provided some invaluable takeaways. Earned media is the most effective way to facilitate brand discovery, with WOM the top channel to discover brands they might not have heard of before. Four-fifths of Chinese consumers discover new brands through earned media channels such as word-of-mouth, consumer review sites and recommendations on social media.

Do not become just a ‘traffic-obsessed brand’

What kind of risks has China’s DTC Disrupters taken that might have turned them into star performers in the short term but pose legitimate concerns of marketing effectiveness in the long run?

Take 5-year-old Perfect Diary success story for example – is it truly a ‘perfect startup’ as imagined, and can its model be an arrow in the quiver for brands outside the beauty and cosmetics category?

Sheldon Li, CEO of Bencross, regards Perfect Diary as a brand accelerated by traffic and a more efficient media strategy to obtain customers faster.

However, “the proportion of research and development in its financial report will determine whether the product is strong enough to support the brand in the future. If its growth path cannot be sustained, it will eventually regress by five years and become a short-lived meteor,” he says.

Industries with fewer dominants are easier to disrupt

Does heritage and size of a brand now matter less to the new-age Chinese consumer? Have DTC disruptors countered these traditional disadvantages of being unknown and insignificant? Yes. Alexander Kremer and Cedric Jäger point to analysis from Big One Labs that shows the concentration of top brands among several FMCG categories on Tmall and JD.

For milk powder, large brands dominate over 80% of the whole category but for general household items, it is just 10%. Also, the gap between the market shares of the Top-10 and Top-50 differs significantly. This becomes obvious in the make-up category where the Top-10 cohort controls 32% and the Top-50 at 62% – a large gap. This means potential for new and smaller entrants that the Chinese term ‘waist-level’ brands (腰部品牌).

Be shapeless and fluid like water

OMD China’s Mimi Lu advocates fluid branding, a fluid omnichannel strategy and fluid segmentation based on small data. The most fluid DTC brands weave imagination into their communications and leave room for interpretation——and even misinterpretation. Ubras’ comedic video leaves people to form their own understandings of the brand. Home Facial Pro sees Little Red Book as a content-seeding channel while using Tmall to gain a greater share of the beauty category at the same time. And ‘small data’ from just 2000 consumers worked wonders for Lemonbox who designed its user experience based on that to deliver customised recommendations of vitamins.

Hire your users as your employees

NaiTangPai’s Michael Zhang shares how he tapped a niche segment in China’s lingerie business and even tapped into his user base to staff a consumer-centric team.

“For example, 60% of our colleagues are from the community. Since our relationship with users has been very strong, we no longer do customer research through third parties, such as focus groups conducted by research companies, but directly through users. In contrast with traditional methods, the connection between the business and the user is more like one between friends and companions,” he says. That is a leg up against most other companies that only have a macroscopic view of market data but lack a micro-understanding of their users and their unmet needs.

Discover, not invent, demand from unmet needs

The best emerging brands that receive commercial favour and media attention are basically doing one thing right – they make excellent products to solve problems that other brands did not care about or did not take seriously in the past. BuffX founder Kang Le reveals how his functional food startup achieved rapid e-commerce success with nutritional gummies that target folks who lack good sleep.

Wanting to educate consumers is entrepreneurial arrogance, he argues. BuffX wants to discover, not invent demand, for unmet needs, especially in ‘uncultivated’ industries like China’s functional food industry. “On the other hand, in a fully saturated and competitive industry like 3Cs (a collective term for computer, communication and consumer electronics products in China), all the more we have to ‘educate’ consumers because most of their needs have been already met.”

Insist on Oriental heritage and artisanal R&D

Chinese make-up brand Florasis’ co-founder Freeman recounts how it rode on the Chinese-ness (国潮) trend to disrupt the market amid stiff competition. The Florasis formulation relies on ancient Chinese recipes to produce cosmetics incorporating flower essences and herbal extracts. Unprecedented products like its fleece flower root eyebrow powdered pencil and its sculpted lipstick with Chinese beauty motifs engraved on the lipstick itself have been co-created with users who evaluate samples and give the company feedback on their experiences. Its virtual persona Hua Xi Zi, launched in June 2021, is also designed to be a personification of Florasis and reflect the brand’s emphasis on traditional Chinese heritage and oriental beauty. The avatar, which shares the same name as the brand, is described to be "like a hibiscus with a unique, natural, confident and elegant temperament" and is a stylish and classical woman with "a head of black diaphanous hair, skin like gelatin, and a little beauty mole at the top of her eyebrows".

Good old customer-centricity never fails

Uki Zhang, Genki Forest’s partner and head of functional brands and products, jokes about making a documentary about the company by just placing a hidden camera in the office. “Our customers would be touched and amazed at how frequently we say “customer-first” in our daily conversations. For example, I told our colleagues, if I don’t give you a single salesperson, and you’re still confident that this product can attract customers, then you launch it,” she said. To further please the customer, Genki Forest also does not have a limit for the R&D department, unlike a lot of companies in the beverage industry facing rigid cost structures for R&D.

Take back control, but don't cut out intermediaries

The brand-consumer relationship has become impersonal ever since e-commerce platforms pose as the intermediary between the two. However, Qumin’s Arnold Ma warns about the risks if brands choose to take the term 'DTC' too literally, and wholly concentrate their efforts on directly-owned channels and direct sales only.

The giant marketplaces, like Tmall and JD.com, provide economies of scale which are difficult and costly for smaller businesses to achieve on their own in China. Despite the fees involved, the connection to a vast audience, data analytics and e-commerce expertise are necessary for many brands trying to gain a foothold in the Chinese e-commerce market. The abovementioned platforms have started offering data-focused solutions to allow brands to get to know their consumers better, albeit at a premium. Both Alibaba’s Tmall Innovation Centre and JD.com’s Consumer-to-Manufacturer service provide sales data and consultancy services. This can be an effective tool: based on JD.com’s insights about consumer demand for nappies that use composite materials, Huggies launched a new range of products which accounted for more than 62% of the brand’s total sales.

Play around with creativity and sustainability

While instant coffee is often seen as cheap compared to a freshly brewed cup of joe, homegrown DTC brand Saturnbird has succeeded in China’s Western-dominated coffee market by eschewing product-focused marketing and instead taking a holistic view to build its brand and create value-added experiences. Saturnbird cultivated ‘fansumers’ by reaching out to vertical interest groups in photography, cookery, illustration and art. WGSN’s Athena Chen also highlighted how it made sustainability fun with 100% recyclable materials and a country-wide recycling programme. In five years, Saturnbird has built a loyal fan base and a strong reputation among Tier 1 cities’ coffee lovers. It replaced Nestle in 2019 to become Tmall’s No 1 coffee brand during Double 11.

Read more in this Spotlight series

Fast-growing brands making fast-moving goods: Why China's FMCG challengers are special

Alexander Kremer and Cedric Jäger

Brand in action: How NaiTangPai made it big with bras

Michael Zhang

DTC disruptors: Consumer sentiment data

Spotlight data report